Black and scholes / Stochastic simulation

SIMULATION OF A BROWNIAN MOTION

## import pandas as pd

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from bokeh.plotting import figure, show, output_file, output_notebook

from bokeh.models import HoverTool

output_notebook() # plot

<!-- <div class="bk-root">

<a href="https://bokeh.pydata.org" target="_blank" class="bk-logo bk-logo-small bk-logo-notebook"></a>

<span id="1001">Loading BokehJS ...</span>

</div> -->

mu, sigma = 0, 1/252

N = 1000

variation = np.random.normal(mu, sigma, N)

bm = np.cumsum(variation)

random_x = np.linspace(0, 1, N)

hover = HoverTool(tooltips=[

("(x,y)", "($x, $y)"),

])

p = figure(plot_width=900, plot_height=400, title= "Brownian motion", tools=[hover])

p.line(random_x, bm)

show(p)

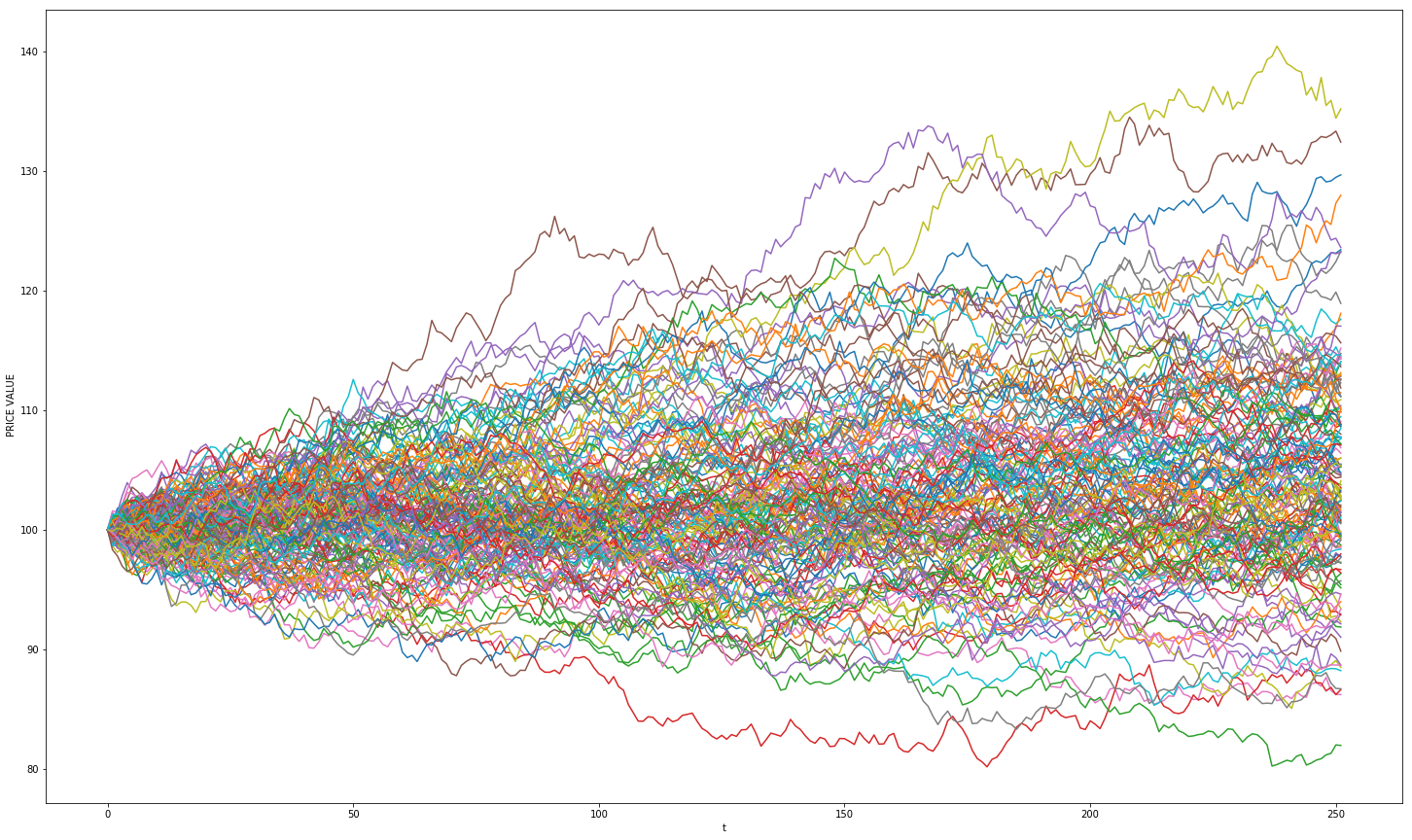

Asset price stochastic path

Suppose that the process followed by the underlying market variable is :

where $dz$ is a Wiener process.

#funtion of asset projection

def stockpaths(S, mu, sigma, T, n):

mat=np.zeros((n, 252))

for i in range(0,n):

mat[i][0] = S

for j in range(1,252):

mat[i][j] = mat[i][j-1]*np.exp(((mu - 0.5*(sigma*sigma))*(T/252)) + (sigma*np.random.normal(0, 1, 1)*np.sqrt(T/252)))

return mat

projections = stockpaths(S=100, mu=0.05, sigma=0.10, T=1, n=150)

#Plot graphics

# Ploting the default graphique

plt.figure(figsize=(25, 15))

plt.plot(pd.DataFrame(projections).transpose())

plt.xlabel('t')

plt.ylabel(' PRICE VALUE')

plt.show()